April Market Update

Disclaimer: All data is sourced from Altus Data Studio, which reports commercial real estate transactions valued at $1,000,000 or more. Information presented reflects activity in the markets of Oakville, Burlington, Mississauga, Milton, and Brampton. Readers are encouraged to verify all details independently before making any real estate decisions.

April 2025 saw mixed results across the western GTA’s commercial real estate markets. While overall transaction volume dropped 25% year-over-year and total sales volume fell nearly 47%, several local markets told a more nuanced story. Mississauga remained strong, led by industrial and retail activity, while Oakville saw a notable spike in industrial sales—largely thanks to new inventory at Three Oaks Business Centre. Burlington and Brampton cooled significantly, both seeing fewer deals across most asset classes. Milton held steady, with signs of renewed interest in development land. Overall, investor caution is still present, but select areas and sectors continue to draw attention.

Key Highlights:

Oakville saw a jump in industrial transactions, though overall dollar volume dropped.

Burlington slowed significantly, with steep declines in sales and volume.

Mississauga remained strong, driven by demand for industrial and retail properties.

Milton held steady in activity, with signs of land interest picking up.

Brampton cooled down, though average prices in industrial held firm.

Average total sales volume is the sum of average sales volume across the 6 asset types. This does not represent the total sales volume of all transactions.

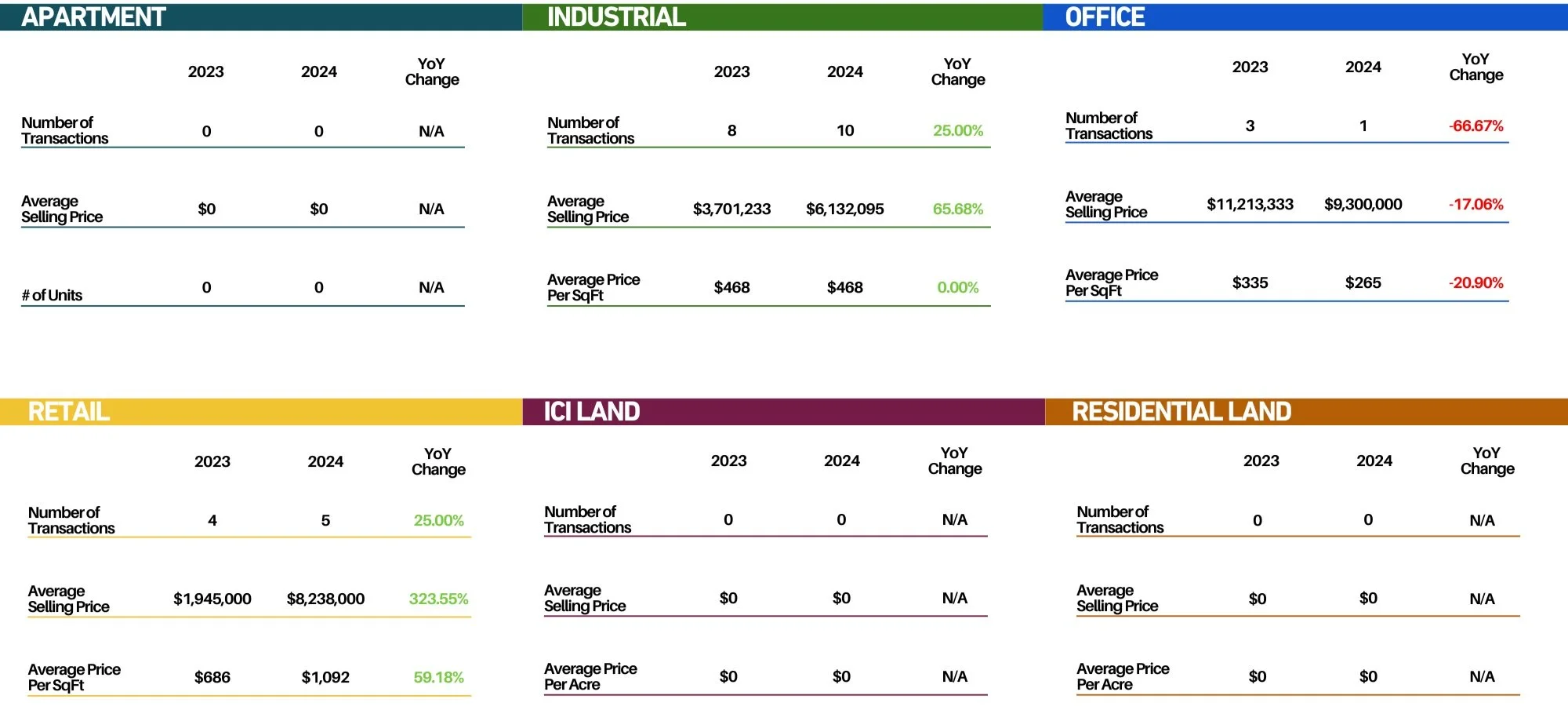

Oakville

Oakville’s commercial market saw a healthy rise in transactional activity, jumping from 8 deals last April to 10 this year — largely driven by a significant uptick in industrial sales. Industrial transactions rose from just 1 in April 2024 to 10 in April 2025, accounting for nearly all of this year’s activity. This spike is largely attributed to Three Oaks Business Centre, a new industrial development in the area, which contributed 7 out of the 10 transactions. Despite the increased deal flow, total average sales volume fell from $24.9M to $9.4M, indicating that the properties sold were smaller or more entry-level units. Meanwhile, retail, office, and land sectors remained quiet this April, potentially reflecting limited inventory or paused investor appetite.

Oakville saw 10 transactions this April compared to 8 transactions last April.

Burlington

Burlington remained relatively quiet but showed signs of modest growth. A new apartment transaction was recorded, andBurlington’s commercial market slowed sharply in April. Transaction volume dropped from 11 deals last year to just 2 this April, with total average sales volume falling by nearly 85%. While most asset classes saw no activity at all, retail remained a modest bright spot — doubling from 1 to 2 sales year-over-year. The sharp decline may reflect a pause in investor confidence or limited inventory available on the market. Whether it’s a temporary blip or part of a broader trend remains to be seen, but buyers appear to be proceeding cautiously for now.

Burlington saw 2 transactions this April compared to 11 transactions last April.

Mississauga

Mississauga continues to show strength across key sectors. The number of transactions edged up slightly from 15 to 16 year-over-year, but total sales volume grew by over 40%, climbing to $23.6M in April 2025. Industrial sales were the biggest driver, rising from 8 to 10 deals and fetching significantly higher average prices. Retail also posted gains, both in transaction count and price per square foot — up over 59%. These metrics reinforce Mississauga’s continued appeal for investors seeking stable assets in a well-established economic hub.

Mississauga saw 16 transactions this April compared to 15 transactions last April.

Milton

Milton’s commercial market held steady with 2 transactions in both April 2024 and April 2025. That said, the types of properties changing hands this year were notably different. Industrial activity disappeared entirely, replaced by one retail and one ICI land deal. While total average volume dropped from $25M to $7M, the price per acre for land jumped by over 200%, suggesting increased interest in future development potential. Investors may be positioning themselves early ahead of long-term servicing plans in the area.

Milton saw 2 transactions this April, the same number as last April.

Brampton

Brampton saw a sharp drop in activity this April, with transactions cut in half — down to 6 from 12 a year ago. Sales volume also slipped slightly, falling 10.7% year-over-year. Most of the movement came from the industrial sector, which remained active with 6 trades, but down from 9 in 2024. Interestingly, the average selling price for industrial assets actually increased slightly, up 8.35%, hinting that buyers are still willing to pay premiums for well-located or higher-quality spaces. Other property types saw no recorded activity this month.

Brampton saw 6 transactions this April compared to 12 transactions last April.